| Consumer Metrics Institute News Feed Subscribe to Consumer Metrics Institute News by Email |

Consumer Metrics Institute

Home of Daily Consumer Leading Indicators

| Consumer Metrics InstituteHome of Daily Consumer Leading Indicators |

| Home | History | Automotive | Entertainment | Financial | Health | Household | Housing | Recreation | Retail | Technology | Travel | FAQs | Downloads | Membership | Contact | About |

| January 29, 2011 - What the BEA's Advance Estimate of Fourth Quarter 2010 GDP Was Really Telling Us: The Bureau of Economic Analysis' ("BEA") "Advance Estimate" of the fourth quarter 2010 Gross Domestic Product ("GDP") had a headline annualized growth rate of 3.17% for the U.S. economy, some 0.62% higher than their estimate of the third quarter's annualized growth rate of 2.55%. It is important to note that historically the BEA eventually adjusts "Advance Estimate" percentages by an average of 1.3% (up or down, with the standard deviation of the adjustments about 1.0%), making all the the below analysis a necessary but possibly meaningless exercise. As a quick reminder, the classic definition of the GDP can be summarized with the following equation: or, as it is commonly expressed in algebraic shorthand: For the fourth quarter of 2010 the values for that equation (total dollars, percentage of the total GDP, and contribution to the final percentage growth number) are as follows: GDP Components Table

The quarter-to-quarter variances in the contributions that the components made were startling, and they can be better understood from the table below that breaks out the component contributions in more detail (and over time). In the table we have further split the "C" component into goods and services, split the "I" component into fixed investment and inventories, separated exports from imports, and listed the quarters in columns with the most current to the left: Quarterly Changes in % Contributions to GDP

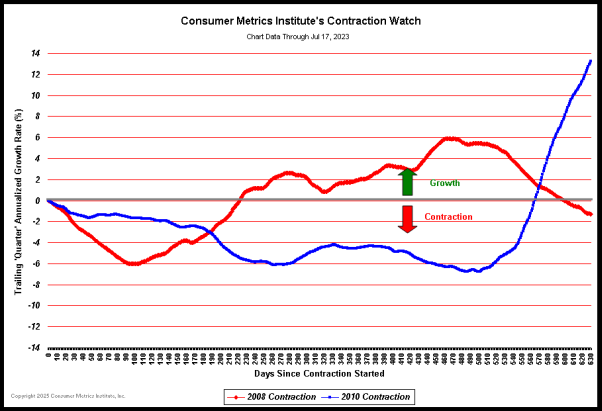

While consumer services and exports remained relatively stable, the growth contributions of the other components changed dramatically. In fact, some of the swings in the component values dwarfed the overall quarter-to-quarter improvement of 0.62%: the changes in trade "added" nearly 5.2% to the total, while the swing in inventories "subtracted" over 5.3%. Statistically it can be challenging to pull legitimate composite signals from this amount of quarter-to-quarter noise. Furthermore, some of the key components (e.g., the trade numbers and inventories) represent, at best, two months of real data plus one month of "guesstimate" -- a perilous task given the rates of change being experienced from quarter to quarter (particularly in the "deflater" being used, as covered below). The "Advance Estimate" will be revised at the end of each of the next two months, and then again in July. One year ago the prior fourth quarter's "Advance Estimate" ultimately ended up being erroneously high by about .7% by the time that the revisions were complete (six months later, at the end of July). Additionally, the reported real (i.e., inflation adjusted) annualized growth rate of 3.17% benefited from a relatively low annualized inflation assumption of 0.3% for the quarter -- which contradicts a number of other current inflation estimates, including the December year-over-year CPI numbers (running 5 times higher at about 1.5%), the PPI finished goods numbers for December (reported to be over 10 times higher at a 4.0% annualized rate) and the BEA's own "deflater" for the prior quarter (which was set 7 times higher at 2.1%). Arguably, a major portion of the 3.17% growth would evaporate if the 0.3% "deflater" proves to be unduly optimistic. Ironically, the flip-side of the low "deflater" being used for the entire economy is the extremely high 21.8% annualized "deflater" that was used to inflation-adjust the amounts of goods that were imported during the quarter. This huge spike in the imported goods "deflater" (up 31% from a -9.2% dis-inflationary number used in the third quarter) partially explains the dramatic drop in reported imports in the GDP equation (and that consequently boosted the overall GDP growth rate by over 4.9%). Given the recent movement in commodity prices (especially oil) it is hard to quarrel with the 21.8% number per se (even if it brings the 0.3% overall "deflater" into question), but the impact of that "deflater" has certainly added to the noise present in this GDP release, if not to the headline number itself. Setting aside for the moment our concerns about the reliability of the data, a face-value read of the report reveals several surprises in the data: ? The inventory building that had been adding significantly to the headline GDP growth rate since the third quarter of 2009 has sharply reversed. This component is generally subject to the largest revisions from release to release, since the data seems to lag more than most of the series. But with that caveat, it is clear on face-value that the five consecutive quarters of inventory building has ended -- perhaps with a vengeance. ? The net growth of governmental spending has also reversed. Given the political environment in Washington and the fiscal realities facing state and municipal governments, that trend is likely real and it will probably stay with us for some time. ? As mentioned above, the BEA reports a contraction in the quantity of imported goods and services by nearly 4%. While a contraction of this magnitude has occurred quarter-to-quarter many times before, it has generally been accompanied by (and ultimately caused by) a sharp contraction in consumer spending. No such change in consumer behavior is even hinted at elsewhere in the report. The only plausible explanation for this contraction is a huge shift in market share from foreign producers to domestic sources. However, no such shift was observed in any of the larger segments of the consumer economy -- including automobiles, apparel, electronics and oil. ? Again at face-value, about a quarter of the annualized growth (or about 0.83%) came from a recovery in residential housing investment, which is reportedly now growing at a tepid 0.08% annualized rate. This was the second positive quarter for residential housing investment during the year (but only the third over the past four years), and portends well for the economy if the reported trend continues. Our concern, however, is that the data used in this series has been subject in the past to short term distortions (e.g., permit rushes to beat code deadlines). ? Consumer spending was reported to have strengthened by about 1.3%, with consumer goods now being shown to be have an annualized growth rate of 2.26%. We would like to believe at face-value the BEA's latest GDP report. However, even if it is absolutely correct, it portrays turbulent undercurrents in this economy that warrant attention: ? The recent round of inventory building is over. Inventory cycles generally run for a number of quarters, with the last building cycle running for 5 consecutive quarters and the last inventory draw-down lasting for 8 consecutive quarters. Inventories are likely to be a drag on the GDP over at least the next year. ? Governmental support of the economy has begun to sharply decrease. Mr. Bernanke notwithstanding, real commerce created by governmental entities has begun to decline, and it is likely to continue to do so for the foreseeable future. ? The recent rapid increase in commodity prices has caused a correspondingly rapid decrease in reported imports. Not reported is what the same rise in commodity prices has done to the purchasing power of consumer take-home pay. If the 31% swing in the quarter-to-quarter price of imported goods is correct, real discretionary consumer spending is about to take a serious hit. Those observations can be drawn from the report if it is taken a face-value. Not obvious from the report itself is a turbulence created by the variance between the past few quarters of GDP reports and the experiences of the un- or under-employed in America. It also portrays a continued and reasonable economic growth that may seem unbelievable to homeowners trapped by their mortgages. It paints a picture of modest prosperity that is probably contrary to the real-world experiences of "Main Street" Americans that on a daily basis drive past strip malls that are at least as "Available" as occupied. Our data continues to indicate that this recession and the much reported recovery (as supported by this GDP report) have not been a shared experience of all Americans. Mr. Bernanke, Mr. Geithner and their colleagues at Goldman Sachs have probably not personally felt the impact of this economic event to the same extent as those of us without privileged access to taxpayer supported defined benefit plans, pay checks backed by self-printed money, zero cost loans or microsecond access to equity market transaction data before those transactions are even executed. The turbulent undercurrents read from the BEA's report don't address the social consequences of a likely widening gap between the rich and poor of this country -- or the young and old. Cultural, racial, gender and educational gaps have probably widened as well -- and we may well be seeing signs of that in our data. Frankly, no amount of slicing or dicing the BEA's numbers can reconcile this "Advance Estimate" report to the behavior of the on-line consumers that we track. Our consumers are still contracting their on-line demand for discretionary durable goods on a year-over-year basis -- and they have now been doing so for more than a year. We have written extensively before on the possible causes for this divergence (see our FAQs for a brief summary of the methodology differences involved and a more detailed discussion of this most recent divergence). We are also keenly aware that our readership may be suffering from "contraction fatigue" and becoming increasingly inclined towards the good news coming out of Washington. Unfortunately, our data is what it is, as our "Contraction Watch" so clearly demonstrates:  (Click on chart for fuller resolution) In the above chart the day-by-day courses of the 2008 and 2010 contractions in our Daily Growth Index are plotted in a superimposed manner with the plots aligned on the left margin at the first day during each event that our Daily Growth Index went negative. The plots then progress day-by-day to the right, tracing out the changes in the daily rate of contraction in consumer demand for the two events. The 2010 contraction event is now more than a year old, dating back to January 15, 2010. Although the chart clearly bottomed at about 9 months into the contraction (at roughly 270 days), the rise since that bottom has been neither steady nor substantial. In fact, there is no way to forecast when the indicated contraction of on-line consumer demand for discretionary durable goods will end based solely on the recent course of the blue line. The above chart speaks to more than the continued possibility of a (now generally dismissed) "double-dip" recession. It indicates that discretionary spending habits have changed (and remain changed) for the demographics that we track. The lingering contraction and near lateral movement of the blue line indicates that modest prolonged year-over-year contraction may be a new "normal" for the economy. If so, this is not something that the vast majority of Americans have ever experienced. Only our grandparents (or our peers in Japan) have seen anything of this sort. Let's hope that the BEA is correct. I'd rather have our data be wrong than to miss an entire decade of growth. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||